A condominium board of directors must comply with Florida Statutes 718.112 section 2a.

2.a. In addition to annual operating expenses, the budget must include reserve accounts for capital expenditures and deferred maintenance. These accounts must include, but are not limited to, roof replacement, building painting, and pavement resurfacing, regardless of the amount of deferred maintenance expense or replacement cost, and any other item that has a deferred maintenance expense or replacement cost that exceeds $10,000. The amount to be reserved must be computed using a formula based upon estimated remaining useful life and estimated replacement cost or deferred maintenance expense of each reserve item. The association may adjust replacement reserve assessments annually to consider any changes in estimates or extension of the useful life of a reserve item caused by deferred maintenance. This subsection does not apply to an adopted budget in which the members of an association have determined, by a majority vote at a duly called meeting of the association, to provide no reserves or less reserves than required by this subsection.

The appraiser’s Reserve Study begins with a comprehensive list of assets costing $10,000 or more that will wear out over time and must be replaced. Each asset has an estimated life and an effective age. The estimated remaining life of the asset tells the amount of time left before replacement of the asset will be required. By Florida law when allocating budget monies, the association’s board of directors must assign a portion of its funds to reserves for roof replacement, building painting and pavement resurfacing. The funds allocated to each asset are determined by its age and years left before it must be replaced. The allocation of funds to reserves is calculated to insure that at the end of their life, there are funds available to replace the roof, repaint the buildings and resurface the pavement.

Example of Reserves: A roof with an estimated cost of replacement of $200,000 is 15 years old. The roof’s life is estimated to be 25 years with 10 years remaining before the roof must be replaced. If there are currently $120,000 in roof reserves, the board must allocate an additional $80,000 over the next 10 years to cover replacement of the roof. In this example the board must place $8,000 in roof reserves each year for the next 10 years to cover the cost of replacing the roof.

The appraiser’s Reserve Study provides the replacement cost information the association’s board needs to calculate the funds that must be placed into reserves for roof replacement, building painting and pavement resurfacing, and other assets.

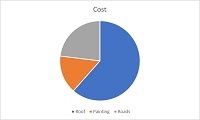

Straight line Reserves: Each asset is treated separately. The amount needed annually for each asset is equal to the amount to put aside in total. Say roof is $8,000, painting is $2,000, and road resurfacing is $3,000, total amount for this year’s budget is $13,000. In straight line reserves the board may only use the reserve amount allocated for that item. For example, the board may not “borrow” from the painting reserve to cover a shortfall for the roof repair. The membership would have to approve any use of allocated straight line reserve funds to replace or repair another asset.

Pooled Reserves: A more complicated calculation that provides more flexibility and generally lowers the annual amount to place in the reserve account. All of the funds are in one account. When an asset needs to be replaced or repaired it is paid for from the account

2.a. In addition to annual operating expenses, the budget must include reserve accounts for capital expenditures and deferred maintenance. These accounts must include, but are not limited to, roof replacement, building painting, and pavement resurfacing, regardless of the amount of deferred maintenance expense or replacement cost, and any other item that has a deferred maintenance expense or replacement cost that exceeds $10,000. The amount to be reserved must be computed using a formula based upon estimated remaining useful life and estimated replacement cost or deferred maintenance expense of each reserve item. The association may adjust replacement reserve assessments annually to consider any changes in estimates or extension of the useful life of a reserve item caused by deferred maintenance. This subsection does not apply to an adopted budget in which the members of an association have determined, by a majority vote at a duly called meeting of the association, to provide no reserves or less reserves than required by this subsection.

2.a. In addition to annual operating expenses, the budget must include reserve accounts for capital expenditures and deferred maintenance. These accounts must include, but are not limited to, roof replacement, building painting, and pavement resurfacing, regardless of the amount of deferred maintenance expense or replacement cost, and any other item that has a deferred maintenance expense or replacement cost that exceeds $10,000. The amount to be reserved must be computed using a formula based upon estimated remaining useful life and estimated replacement cost or deferred maintenance expense of each reserve item. The association may adjust replacement reserve assessments annually to consider any changes in estimates or extension of the useful life of a reserve item caused by deferred maintenance. This subsection does not apply to an adopted budget in which the members of an association have determined, by a majority vote at a duly called meeting of the association, to provide no reserves or less reserves than required by this subsection. The appraiser’s Reserve Study begins with a comprehensive list of assets costing $10,000 or more that will wear out over time and must be replaced. Each asset has an estimated life and an effective age. The estimated remaining life of the asset tells the amount of time left before replacement of the asset will be required. By Florida law when allocating budget monies, the association’s board of directors must assign a portion of its funds to reserves for roof replacement, building painting and pavement resurfacing. The funds allocated to each asset are determined by its age and years left before it must be replaced. The allocation of funds to reserves is calculated to insure that at the end of their life, there are funds available to replace the roof, repaint the buildings and resurface the pavement.

The appraiser’s Reserve Study begins with a comprehensive list of assets costing $10,000 or more that will wear out over time and must be replaced. Each asset has an estimated life and an effective age. The estimated remaining life of the asset tells the amount of time left before replacement of the asset will be required. By Florida law when allocating budget monies, the association’s board of directors must assign a portion of its funds to reserves for roof replacement, building painting and pavement resurfacing. The funds allocated to each asset are determined by its age and years left before it must be replaced. The allocation of funds to reserves is calculated to insure that at the end of their life, there are funds available to replace the roof, repaint the buildings and resurface the pavement.  Straight line Reserves: Each asset is treated separately. The amount needed annually for each asset is equal to the amount to put aside in total. Say roof is $8,000, painting is $2,000, and road resurfacing is $3,000, total amount for this year’s budget is $13,000. In straight line reserves the board may only use the reserve amount allocated for that item. For example, the board may not “borrow” from the painting reserve to cover a shortfall for the roof repair. The membership would have to approve any use of allocated straight line reserve funds to replace or repair another asset.

Straight line Reserves: Each asset is treated separately. The amount needed annually for each asset is equal to the amount to put aside in total. Say roof is $8,000, painting is $2,000, and road resurfacing is $3,000, total amount for this year’s budget is $13,000. In straight line reserves the board may only use the reserve amount allocated for that item. For example, the board may not “borrow” from the painting reserve to cover a shortfall for the roof repair. The membership would have to approve any use of allocated straight line reserve funds to replace or repair another asset. Pooled Reserves: A more complicated calculation that provides more flexibility and generally lowers the annual amount to place in the reserve account. All of the funds are in one account. When an asset needs to be replaced or repaired it is paid for from the account

Pooled Reserves: A more complicated calculation that provides more flexibility and generally lowers the annual amount to place in the reserve account. All of the funds are in one account. When an asset needs to be replaced or repaired it is paid for from the account